Institutional Self-Harm or Institutional Self-Rescue? 制度性自殘,還是制度性自救? ——The Tariff Authority Dispute Involves the Correlation Between Procedural Justice and Government Efficiency

——關稅權之爭涉及程序正義與政府效率相關性 錢 宏 Archer Hong Qian (Intersubjective Symbiosism Founation) 摘要 關稅權本是政府首腦的行政權,而非單純立法權。美國自建國以來,關稅事務一直歸屬總統與財政部管理,從未設立獨立“海關總署”。假設最高法院裁定對美國國際貿易法院和聯邦巡迴法院判決川普總統關稅權“無效”,這已超出“三權分立”的制度設置爭論,直指美國能否在國際貿易中快速捍衛國家利益。若剝奪總統關稅裁量,就是制度性自殘;若在憲制框架下保留適度權能,則是制度性自救。 關鍵詞 關稅權;三權分立;國家利益;制度經濟學;美國海關歷史;制度性自殘自救;化解“國際不對等+行政反應遲緩”的兩難;“關稅權”的邏輯鏈條;“制度性不對稱”的國際解法;《緊急互惠關稅權法》(草案)

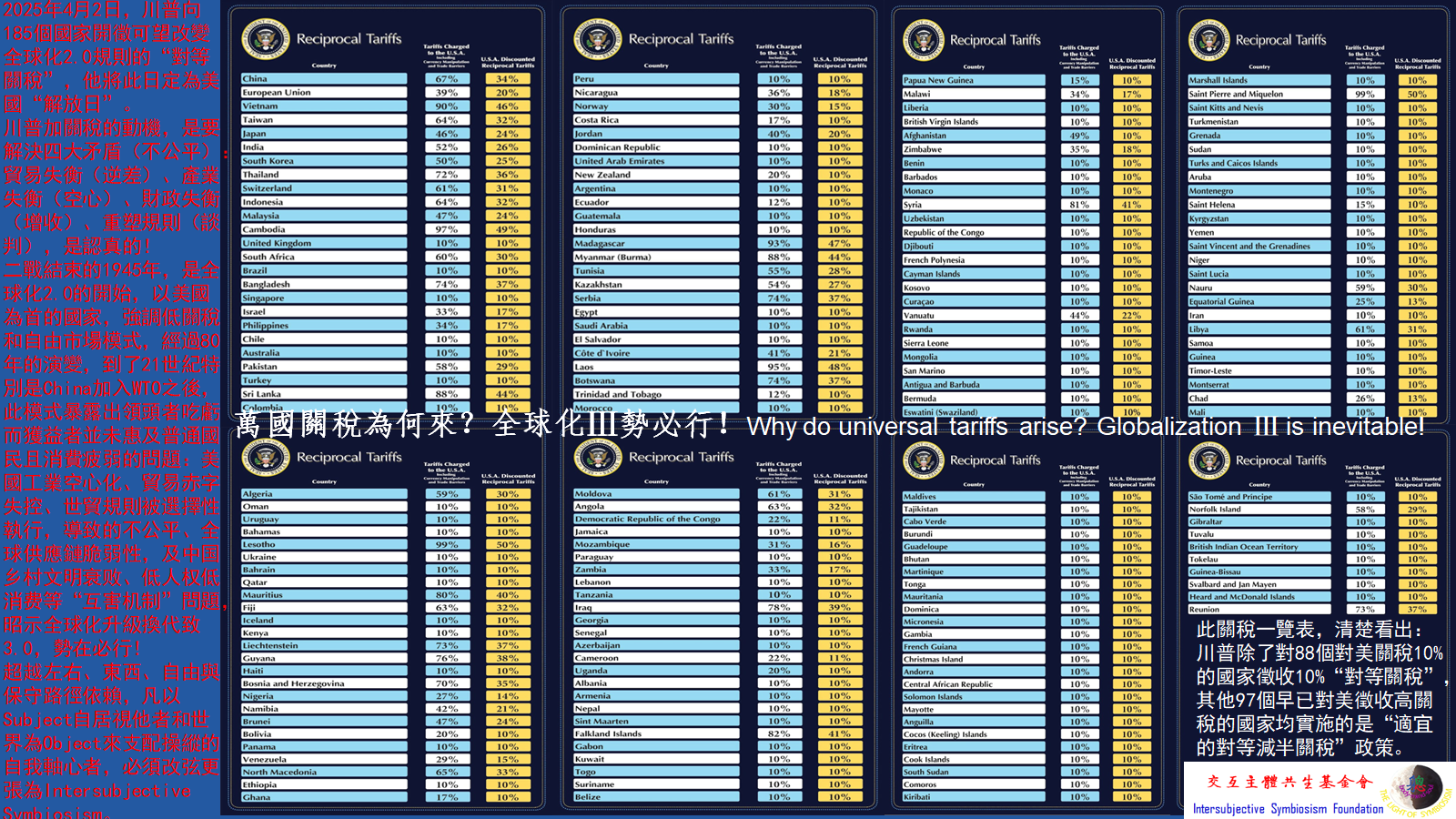

目錄 本文背景 一、海關的歷史常識:從“行關文”到“行關稅” 二、美國特殊情況及海關歷史:三權分立與關稅權之爭 三、司法裁決與制度性風險 四、專門化解“國際不對等+行政反應遲緩”的兩難 五、“制度性不對稱”的國際解法(外部配套) 六、總結:“關稅權”的邏輯鏈條(從行政合法性到政府 附錄:《緊急互惠關稅權法》(Emergency Reciprocity Authority Act, ERAA)草案提綱(便於政策溝通運行) 本文背景 川普總統以“萬國互惠關稅”的方式,解決“特利芬-羅德里斯三元難題”條件下經濟全球化(2.0)出現的國際貿易中對美貿易出現的“不公平”“非對等”問題,十分必要,不僅促使全球貿易規則重組(全球化3.0),而且,在相當長一段時間內可以增加美國政府的收益,四個多月來,這項政策已經取得“公平”與“減赤”雙重針對性的顯著成效。美國貿易法院(U.S. Court of International Trade)和美國聯邦巡迴法院(U.S. Court of Appeals for the Federal Circuit),受理國內某些企業起訴,判川普對等關稅政策不合美國國內法“程序正義”,稱關稅權不屬於總統,有待最高法院終審判決。我相信美國這兩個法院的法官,不會傻逼到不管不顧美國人民和國家整體利益,但這裡就有了一對小小矛盾:“國際貿易公平與國內程序正義”如何調節?

一、海關的歷史常識:從“行關文”到“行關稅” 早期“關文”——行政許可

在古代,海關最早的功能是“通行許可”。“關”就是關卡、邊防口岸,主要任務是 檢查和放行貨物、人群,收取一定的“通關文牒”費用。 這一制度在中國、西方都有。中國漢唐就有“過所”“關牒”,歐洲中世紀各諸侯國也設關卡收過境費。 性質:行政行為,由君主或地方長官命令設立,並不需要議會立法批准。

近代“關稅”——財政與貿易調節工具

進入近代以後,尤其是16–18世紀,隨着國際貿易興起,關卡逐漸演化為 國家財政和產業政策的重要來源。 中國明清時,“海關稅收”成為中央財政的重要組成部分;歐洲各國通過關稅保護國內產業。 無論中西,關稅的徵收權仍然主要體現為 政府的行政權力,因為其直接由國王/皇帝/內閣行使,屬於財政收支的組成部分。 議會或代議機構頂多起到 批准預算或監督財政 的作用,而不是直接操作“行關稅”。

國際比較與制度本質

中國與大陸傳統:1)、無論古代還是今天,中國的海關完全是行政機關,由中央政府設立、管理和調整關稅政策;2)、 關稅政策屬於財政部+海關總署的一體化操作,立法機關(全國人大)一般不直接介入。 歐洲傳統:1)、英國、法國等國,議會對關稅有一定立法監督,但主要體現在稅收法案的批准;2)、實際操作權仍在行政部門(財政部或海關局)。 美國的“混合模式”:1)、憲法把關稅設為國會的權力,反映了當時“無代表,不納稅”的獨立革命精神;2)、但現代化以來,國會通過法律授權,已把絕大部分操作權交給總統和行政機關;3)、名義上屬立法權,實質上屬行政權。 從世界歷史看,從“行關文”到“行關稅”,都延續了一個邏輯:關稅屬於國家行政權(尤其是財政行政權),不是立法機關的細分領域。 二、美國特殊情況及海關歷史:三權分立與關稅權之爭 關稅政策在歷史實踐上本質是行政權延伸。 憲法上的規定

美國憲法第一條第八款明確規定:國會有權徵收關稅(Duties, Imposts, Excises)。這是因為當時美國建國初期,關稅是聯邦政府最主要的財政來源,所以制憲者把它放在國會(立法機關)手裡,以確保“稅收必須經過人民代表同意”。 但美國沒有獨立的“海關總署”:憲法同時允許國會把部分權力授權給總統。

總統的“行政裁量”

美國有海關與邊境保護局(CBP),隸屬國土安全部,是一個典型的行政機關,負責執行關稅和進出口管制,海關事務始終處於行政體系,受總統政府直接管控。 總統在關稅政策上的權力,主要來源於國會授予的法律授權; 《貿易擴展法》(Trade Expansion Act, 1962)第232條,允許總統以“國家安全”為由調整關稅; 《貿易法》(Trade Act, 1974)第301條,允許總統因“不公平貿易行為”加征關稅; 關稅減免、豁免和具體實施細節,通常由行政部門直接執行。 因此,美國的實際操作是:國會立法設定框架,總統和行政機關根據實際情況執行與調整。

立法與實踐案例

1789年:第一屆國會通過《關稅法》,設立財政部,海關事務歸其直接管轄; 1789—1927年:各大港口由總統任命關長,屬行政任命; 1927年:成立 美國關稅局(U.S. Customs Service),隸屬財政部; 2003年:重組為 美國海關與邊境保護局(CBP),併入國土安全部。 2018年川普總統援引《貿易擴展法》第232條,對鋼鐵和鋁產品加征關稅,這是典型的行政權直接操作關稅。 拜登政府在2022年維持甚至擴大對華關稅,也沒有走國會立法程序,而是延續總統的行政裁量。 可見,美國雖然在憲法上強調國會對關稅的立法權,但在現代國際貿易關係中,總統已實質掌握關稅政策主動權。

總之,海關與關稅,不只是抽象立法,而是直接服務於國家財政與國際交往的工具與國家行政長官的權能。 三、司法裁決與制度性風險 美國最高法院對總統關稅權的裁決,將聚焦於“形式與實質”: 形式:關稅是國會立法權還是總統行政權? 實質:總統在應對不公平貿易時是否擁有快速反應能力? 若裁決收窄總統權力,將使美國在國際博弈中處於制度性不對等地位。 在國際貿易中,若各國行政長官擁有不同層級的關稅權能,制度不對稱就意味着國家利益自我削弱: 如果美國總統的關稅權被過度限制,出現制度性自殘,那麼受益者是誰? 國際競爭對手:

國內既得利益集團:

而真正受傷的,則是美國的整體國家利益:製造業空心化、就業機會減少、國家戰略空間縮小、國際貿易規則的破壞。 因此,關稅權的核心,不僅僅是“權力如何分立”的制度設計問題,更是國家如何在國際秩序中有效自我防衛的根本問題,而且是美國作為文明國家對於國際貿易規則和“全球化重組”的示範性意義——如何再次偉大的問題。 四、專門化解“國際不對等+行政反應遲緩”的兩難 制度性自殘,還是制度性自救?這是美國今天必須回答的抉擇。 讓我們回到“無代表,不納稅”原則(No Taxation without Representation)→三權分立制度(Separation of Powers)→關稅權的歸屬(Tariff Power)三大關聯項,繼續討論在可操作的制度與流程上,如何解決“關稅權”歸屬在實際運用中存在的問題? 1、目標與約束(從原則到邊界) 代議正當性(No Taxation without Representation):關稅屬於稅負的一種,源頭權在國會(美國憲法第一條第八款)。任何讓總統迅速行動的安排,都必須建立在國會事先授權或事後可控的基礎上。constitution.congress.gov 分權制衡(Separation of Powers):允許行政機關“快”,但必須有明晰授權、事實認定、可訴可審的圍欄,避免越權或程序瑕疵被法院推翻(近年在232、301、乃至以IEEPA為依據的訴訟都給出過教訓與啟示)。Justia Lawcafc.uscourts.gov+1Justia法律 國際競爭有效性:對手可以“秒級”響應時,美國若層層緩慢就構成“制度性自殘”。因此需要快觸發 + 強監督的組合,而不是“要麼極慢、要麼越權”的二選一。近來的IEEPA判例趨勢也提示:別把IEEPA當作一般性關稅法用,應回到或更新專門授權路徑。AP NewsReutersThe Washington Post 2、一套可落地的制度組合(Fast-Fair Tariff Architecture, “FFTA”) 1)、預授權:建立“緊急互惠關稅權”(Emergency Reciprocity Authority, ERA)專章立法 由國會專門立法授予總統一項限時、限域、可審的快速關稅權,用來應對對等性失衡與突髮型不公平: A、觸發要件(必須寫入法條):明確列舉的客觀指標(如對方加權有效關稅/非關稅壁壘指數、受補貼傾銷判定、強制技術轉移、國家安全相關供給鏈風險等),一旦超過閾值即可觸發;指標與證據由商務部/ITC/USTR出具即時性“初步認定報告”,附最低限度公開數據。 B、關稅幅度與“互惠公式”:法律中預設“互惠調節公式”(例如把美國對該類產品的適用稅率錨定為對方對等產品的實際障礙強度,並設定法定上限與階梯“snapback”)。 C、時效與日落:先行生效90–180天(總統可立即發布),到期自動失效,除非國會以快速程序表決通過延長/調整;每次延長鬚有更新事實記錄與影響評估。 D、國會快速監督:強制48小時內通報“四大貿易/財政委員會”;15–30天內舉行聽證;設定快速“批准/否決”程序(類比《國會審查法》與貿易快審機制),保障“無代表,不納稅”的民主控制。 註:此路與現有232(國家安全)、201(保障措施)、301(應對不公平做法)並行不悖,但不再濫用IEEPA(國際緊急經濟權力法)。Justia LawAkin - Akin, an Elite Global Law Firmbutzel.com 2)、程序正義與可訴性:把“快”做在前,把“穩”做在後 A、緊急情形的最小程序:公布要點理由書與核心證據表(可作適度保密處理),同步開啟7天簡式意見窗口;30天內發布正式答覆與修訂,把行政記錄補充完整,以經受APA(行政程序法)與CIT/CAFC審查(301案的來回“發回重審—維持”就凸顯了記錄與論證的重要性)。Justia法律cit.uscourts.gov B、專屬且提速的司法通道:指定國際貿易法院(CIT)為一審專屬管轄,60–90天加速審理;上訴到聯邦巡迴同樣走加速軌;立法明確審查標準(如“是否逾越授權”“是否缺乏理性解釋”),減少法庭對“程序/權限”反覆拉扯造成的政策停擺。 C、“持續行動”條款:借鑑Transpacific對232“持續行動”理解,在新法中明確允許在同一事實認定周期內按預設條件做後續微調,避免因“時限/形式”問題被推翻。cafc.uscourts.govSteptoestudentbriefs.law.gwu.edu 3)、代表性與透明度:把“無代表,不納稅”嵌進執行層面 A、必備的國會報告包:影響評估(消費者價格、就業、供應鏈安全與盟友影響)、互惠指數變化、替代政策對比; B、州際均衡說明(憲法“統一稅則”地理均一性的現代理解),與弱勢行業/小企業的配套減負與轉崗支持。constitution.congress.gov 4)、與既有法律的分工協同(少走IEEPA,多用專法) A、232(國家安全):在能源、關鍵礦產、國防工業鏈等安全敏感品類優先用232(其合憲授權基礎較穩固)。Justia LawAkin - Akin, an Elite Global Law Firmbutzel.com B、201(保障)/ 701-731(反補貼/反傾銷):用於行業受損與不公平定價場景; C、301(系統性不公平做法):保留,但必須嚴格APA記錄與意見答覆(CIT在301清單案的審查路徑已給出合格範式)。Justia法律cit.uscourts.gov D、IEEPA:僅限制裁/禁運等傳統用途,不宜作為普遍性關稅法源(近期多案判決趨勢不利)。AP NewsReutersThe Washington Post 五、“制度性不對稱”的國際解法(外部配套) 1.“互惠准入協定”(RAA)與“自動回擺”條款:與主要夥伴(歐盟、日本、英、加、越等)簽署多邊/復邊互惠協議,採用同一“互惠公式”與自動snapback,把臨時關稅變成規則化的合約回應,減少WTO爭端不確定性。 2.把關稅與補貼紀律聯動:將產業補貼、國企中性、數據/技術強迫轉移納入同一互惠框架,形成“障礙—關稅—補救”的閉環。 3.WTO路徑的合規設計:優先走AD/CVD/保障措施與條約性豁免,慎用國家安全例外,降低“報復—反報復”循環。 4.場景化示例(工作流):1)、USTR/商務部每季更新“互惠失衡清單”→發現某國在關鍵品類的有效障礙指數跨閾值;2)、總統依ERA發布臨時互惠關稅(即時生效),同時披露要點理由書並開啟7日意見收集;3、15–30天國會聽證 + 快速表決通道啟動;4)、行政機關發布正式理由與微調,完善記錄;5)若被訴,走CIT加速審理;90–180天窗口期滿後,除非國會通過繼續決議,否則自動日落。 總之,這套解法“快而不失正當”: 速度:總統擁有即時觸發的工具,應對對手“秒級”動作; 合法性:源自國會預授權 + 快速監督 + 強制理由公開 + 可訴可審; 可持續:與232/301/AD-CVD並行不衝突,把IEEPA爭議邊緣化,符合近年的司法走向;AP NewsReutersJustia LawJustia法律 可複製到多國博弈:通過互惠公式與復邊協議,把一次次“個案談判”變成“規則化自動重組”。

六、總結:“關稅權”的邏輯鏈條(從行政合法性到政府效率) 關稅權的運行邏輯Fast-Fair Tariff Architecture (FFTA)圖解: ┌─────────────────────┐ │ LEGITIMACY 合法性 │ ← “無代表,不納稅” │ Taxation = Representation │ 國會為源頭(憲法 I-8) └─────────┬──────────┘ │ 預授權 (Delegation) ┌─────────▼──────────┐ │ DELEGATION 授權 │ ← 國會立法預設緊急互惠關稅權(ERA) │ - 明確觸發條件 │ - 互惠公式 & 上限 │ - 限時/日落條款 └─────────┬──────────┘ │ 程序圍欄 (Guardrails) ┌─────────▼──────────┐ │ GUARDRAILS 圍欄 │ ← 三權分立中的司法與監督 │ - 必須公示理由書 │ - 7日意見 & 30日修訂 │ - 國會快速表決通道 │ - CIT/CAFC加速審理 └─────────┬──────────┘ │ 行動力 (Speed) ┌─────────▼──────────┐ │ SPEED 速度 │ ← 行政即時觸發 │ - 總統180-360日快速關稅 │ - 即時互惠回擺(snapback) │ - 自動到期 unless國會延長 合法性 → “無代表,不納稅”原則;授權 → 國會事先立法設定ERA;圍欄 → 程序正義、司法審查、國會監督;速度 → 總統可立即實施,保障國家利益 附錄:《緊急互惠關稅權法》(Emergency Reciprocity Authority Act, ERAA)草案提綱(便於政策溝通運行) 第一章 總則 第二章 國會預授權 第3條 【授權範圍】總統可在以下情形觸發緊急互惠關稅: 他國實施實質性關稅或非關稅壁壘; 存在補貼傾銷、強制技術轉移或關鍵產業安全風險。

第4條 【互惠公式】關稅幅度按“對方障礙強度”設定,並不得超過本法規定上限。 第5條 【時效條款】措施自發布之日起生效180日,延長不得超過360日;到期自動失效,除非國會表決延長。

第三章 程序與監督 第6條 【理由公開】總統發布關稅時,須同時公布要點理由書與核心證據表。 第7條 【意見徵集】自發布之日起7日內開放意見徵集,30日內發布修訂。 第8條 【國會監督】48小時內通知四大貿易/財政委員會;15–30日內必須舉行聽證並快速表決。

第四章 司法審查 第五章 附則 孞烎2025年9月1日草於Richmond心約開關居

Institutional Self-Harm or Institutional Self-Rescue? ——The Tariff Authority Dispute Involves the Correlation Between Procedural Justice and Government Efficiency By Archer Hong Qian (Intersubjective Symbiosism Foundation) #### Abstract Tariff authority is inherently the executive power of the head of government, rather than purely legislative power. Since the founding of the United States, tariff affairs have always been under the management of the President and the Treasury Department, without establishing an independent "Customs Administration." Assuming the Supreme Court rules on the judgments of the U.S. Court of International Trade and the U.S. Court of Appeals for the Federal Circuit that President Trump's tariff authority is "invalid," this goes beyond the institutional debate over "separation of powers" and directly questions whether the U.S. can swiftly defend national interests in international trade. Stripping the President of tariff discretion would be institutional self-harm; retaining appropriate authority within the constitutional framework would be institutional self-rescue. #### Keywords Tariff authority; separation of powers; national interests; institutional economics; history of U.S. customs; institutional self-harm and self-rescue; resolving the dilemma of "international asymmetry + sluggish administrative response"; the logical chain of "tariff authority"; international solutions to "institutional asymmetry"; Draft of the "Emergency Reciprocity Tariff Authority Act" #### Table of Contents Background of This Article Historical Common Knowledge of Customs: From "Travel Customs Documents" to "Customs Tariffs"

Special Circumstances in the U.S. and History of Customs: Separation of Powers and the Tariff Authority Dispute

III. Judicial Rulings and Institutional Risks Specifically Resolving the Dilemma of "International Asymmetry + Sluggish Administrative Response"

International Solutions to "Institutional Asymmetry" (External Support)

Summary: The Logical Chain of "Tariff Authority" (From Administrative Legitimacy to Government Efficiency)

Appendix: Outline of the Draft "Emergency Reciprocity Tariff Authority Act" (Emergency Reciprocity Authority Act, ERAA) (For Facilitating Policy Communication and Operation) #### Background of This Article President Trump is addressing the "unfair" and "non-reciprocal" issues in U.S. trade arising from economic globalization (2.0) under the conditions of the "Triffin-Rodrik trilemma" through the method of "universal reciprocal tariffs." This is an absolutely necessary measure, not only promoting the reorganization of global trade rules (Globalization 3.0), but also significantly increasing the U.S. government's revenue over a considerable period. Over the past four months, this policy has already achieved notable results targeting both "fairness" and "deficit reduction." The U.S. Court of International Trade and the U.S. Court of Appeals for the Federal Circuit have accepted lawsuits from certain domestic enterprises, ruling that Trump's reciprocal tariff policy violates U.S. domestic law on "procedural justice," claiming that tariff authority does not belong to the President, pending a final decision from the Supreme Court. I believe the judges of these two U.S. courts will not be foolish enough to disregard the overall interests of the American people and nation, but this presents a minor contradiction: How to balance "international trade fairness and domestic procedural justice"? #### I. Historical Common Knowledge of Customs: From "Travel Customs Documents" to "Customs Tariffs" Early "Customs Documents" — Administrative Permits

In ancient times, the earliest function of customs was "passage permits." "Customs" refers to checkpoints and border ports, with the main tasks of inspecting and releasing goods and people, collecting certain "customs clearance document" fees.

Modern "Tariffs" — Tools for Fiscal and Trade Regulation

In the modern era, especially from the 16th to 18th centuries, with the rise of international trade, checkpoints gradually evolved into important sources of national revenue and industrial policy.

In both East and West, the authority to levy tariffs remained primarily an executive power of the government, as it was directly exercised by kings/emperors/cabinets and was part of fiscal revenues and expenditures.

International Comparisons and Institutional Essence

China and Continental Tradition: 1) Whether in ancient times or today, China's customs is entirely an administrative agency, established, managed, and adjusted by the central government for tariff policies; 2) Tariff policies are integrated operations of the Ministry of Finance + General Administration of Customs, with the legislative body (National People's Congress) generally not directly intervening. European Tradition: 1) In countries like Britain and France, parliaments have certain legislative oversight over tariffs, but mainly in approving tax bills; 2) Actual operational authority remains with administrative departments (Ministry of Finance or Customs Bureau). U.S. "Hybrid Model": 1) The Constitution designates tariffs as congressional legislative power, reflecting the "no taxation without representation" spirit of the independence revolution at the time; 2) But since modernization, Congress has delegated most operational authority to the President and executive agencies through laws; 3) Nominally legislative power, but substantively executive power. From world history, from "travel customs documents" to "customs tariffs," a logic has been continued: Tariffs belong to national executive power (especially fiscal executive power), not a subdivided field of legislative bodies. #### II. Special Circumstances in the U.S. and History of Customs: Separation of Powers and the Tariff Authority Dispute Tariff policies, in historical practice, are essentially extensions of executive power. Constitutional Provisions

The U.S. Constitution, Article I, Section 8, explicitly states: Congress has the power to levy tariffs (Duties, Imposts, Excises). This is because in the early days of the U.S. founding, tariffs were the primary source of federal government revenue, so the framers placed it under Congress (the legislative branch) to ensure "taxation must be approved by representatives of the people."

Presidential "Executive Discretion"

The U.S. has the Customs and Border Protection (CBP), affiliated with the Department of Homeland Security, which is a typical executive agency responsible for enforcing tariffs and import/export controls. Customs affairs have always been within the executive system, under direct control of the presidential administration.

Legislative and Practical Cases

It can be seen that although the U.S. emphasizes congressional legislative power over tariffs in the Constitution, in modern international trade relations, the President has substantially held the initiative in tariff policies.

In summary, customs and tariffs are not just abstract legislation but tools directly serving national finances and international relations, as well as the authority of national administrative leaders. #### III. Judicial Rulings and Institutional Risks The U.S. Supreme Court's ruling on presidential tariff authority will focus on "form and substance": Form: Is tariff authority congressional legislative power or presidential executive power? Substance: Does the President possess rapid response capabilities when addressing unfair trade? If the ruling narrows presidential power, it will place the U.S. in an institutionally asymmetric position in international competition. In international trade, if administrative leaders of various countries possess different levels of tariff authority, institutional asymmetry means weakening of national interests: If the President's tariff authority is excessively restricted, leading to institutional self-harm, then who benefits? International competitors:

For example, countries benefiting from subsidies, dumping, currency manipulation, etc.

Domestic vested interest groups:

The true losers are the overall national interests of the U.S.: hollowing out of manufacturing, reduced job opportunities, shrinking strategic space, and disruption of international trade rules. Therefore, the core of tariff authority is not merely a question of "how power is divided" in institutional design, but a fundamental issue of how a nation effectively defends itself in the international order. Moreover, it is the demonstrative significance of the U.S. as a civilized nation for international trade rules and "globalization reorganization"—how to be great again. #### IV. Specifically Resolving the Dilemma of "International Asymmetry + Sluggish Administrative Response" Institutional self-harm or institutional self-rescue? This is the choice the U.S. must answer today. Let us return to the "no taxation without representation" principle (No Taxation without Representation) → separation of powers system (Separation of Powers) → three major linkages of tariff authority attribution (Tariff Power), and continue discussing how to resolve the issues in the operational system and process of "tariff authority" attribution? Goals and Constraints (From Principles to Boundaries)

Representational Legitimacy (No Taxation without Representation): Tariffs are a form of tax burden, with the source authority in Congress (U.S. Constitution Article I, Section 8). Any arrangement allowing the President to act swiftly must be based on prior congressional authorization or post-event controllability. constitution.congress.gov Separation of Powers (Separation of Powers): Allowing the executive branch to be "fast," but must have clear authorizations, fact-finding, appealable and reviewable fences to avoid overreach or procedural flaws being overturned by courts (recent lessons from lawsuits based on 232, 301, and even IEEPA). Justia Law cafc.uscourts.gov +1 Justia Law International Competitive Effectiveness: When opponents can respond at "second-level," if the U.S. is layered and slow, it constitutes "institutional self-harm." Therefore, a combination of fast triggers + strong supervision is needed, rather than the binary choice of "either extremely slow or overreaching." Recent IEEPA rulings also suggest: Don't use IEEPA as a general tariff law; should return to or update specific authorization paths. AP News Reuters The Washington Post A Set of Implementable Institutional Combinations (Fast-Fair Tariff Architecture, "FFTA")

1) Pre-Authorization: Establish a specialized chapter legislation granting the President a time-limited, domain-limited, reviewable fast tariff authority to address reciprocity imbalances and sudden unfair practices: Trigger Requirements (Must be Written into the Law): Clearly enumerated objective indicators (such as the other party's weighted effective tariff/non-tariff barrier index, subsidized dumping determination, forced technology transfer, national security-related supply chain risks, etc.), which can be triggered once exceeding the threshold; indicators and evidence are issued by the Department of Commerce/ITC/USTR with immediate "preliminary determination reports," attached with minimum public data.

Tariff Amplitude and "Reciprocity Formula": Pre-set "reciprocity adjustment formula" in the law (for example, anchoring the U.S. applicable tax rate for such products to the actual barrier intensity of the other party's equivalent products, and setting statutory upper limits and tiered "snapback").

Time Limit and Sunset: Take effect first for 90–180 days (President can issue immediately), automatically expire upon expiration unless Congress passes an extension/adjustment through fast procedures; each extension must have updated fact records and impact assessments.

Congressional Fast Oversight: Mandatory notification within 48 hours to the "four major trade/finance committees"; hold hearings within 15–30 days; set fast "approval/veto" procedures (similar to the Congressional Review Act and trade fast-track mechanisms), ensuring democratic control of "no taxation without representation."

Note: This path runs parallel to existing 232 (national security), 201 (safeguards), 301 (unfair practices), but no longer abuses IEEPA (International Emergency Economic Powers Act). Justia Law Akin - Akin, an Elite Global Law Firm butzel.com 2) Procedural Justice and Appealability: Put "fast" in front, put "stable" in back Minimum Procedures for Emergency Situations: Publish key reasons documents and core evidence tables (can be appropriately classified), simultaneously open a 7-day simplified opinion window; release formal responses and revisions within 30 days, supplement administrative records completely to withstand APA (Administrative Procedure Act) and CIT/CAFC reviews (the back-and-forth "remand-uphold" in 301 cases highlights the importance of records and arguments). Justia Law cit.uscourts.gov

Dedicated and Accelerated Judicial Channels: Designate the Court of International Trade (CIT) as exclusive first-instance jurisdiction, with accelerated hearings in 60 days; appeals to the Federal Circuit also follow accelerated tracks; legislation clarifies review standards (e.g., "whether exceeding authorization," "whether lacking rational explanation"), reducing policy halts caused by courts repeatedly pulling on "procedure/authority."

"Ongoing Action" Clause: Drawing from Transpacific's understanding of 232 "ongoing actions," explicitly allow follow-up fine-tuning under preset conditions within the same fact determination cycle in the new law, avoiding invalidation due to "time limits/forms." cafc.uscourts.gov Steptoe studentbriefs.law.gwu.edu

3) Representativeness and Transparency: Embed "No Taxation Without Representation" into the Execution Level Mandatory Congressional Report Packages: Impact assessments (consumer prices, employment, supply chain security and ally impacts), reciprocity index changes, alternative policy comparisons;

Interstate Equity Explanations (Modern understanding of the Constitution's "uniform tax rules" geographic uniformity), with supporting burden reductions and job transition support for disadvantaged industries/small businesses. constitution.congress.gov

4) Division of Labor and Coordination with Existing Laws (Less Use of IEEPA, More Use of Specialized Laws) 232 (National Security): Prioritize use in security-sensitive categories such as energy, critical minerals, defense industrial chains, etc. (Its constitutional authorization foundation is relatively stable). Justia Law Akin - Akin, an Elite Global Law Firm butzel.com

201 (Safeguards)/701-731 (Countervailing Duties/Anti-Dumping): Used for industry damage and unfair pricing scenarios;

301 (Systematic Unfair Practices): Retained, but must strictly follow APA records and opinion responses (CIT's review path in 301 list cases has provided a qualified paradigm). Justia Law cit.uscourts.gov

IEEPA: Limited to traditional uses such as sanctions/embargoes, not suitable as a general tariff source (Recent multiple rulings trend unfavorable). AP News Reuters The Washington Post

#### V. International Solutions to "Institutional Asymmetry" (External Support) "Reciprocity Access Agreements" (RAA) and "Automatic Snapback" Clauses: Sign multilateral/plurilateral reciprocity agreements with major partners (EU, Japan, UK, Canada, Vietnam, etc.), adopting the same "reciprocity formula" and automatic snapback, turning temporary tariffs into rule-based contractual responses, reducing WTO dispute uncertainties.

Linking Tariffs with Subsidy Disciplines: Incorporate industrial subsidies, state-owned enterprise neutrality, data/technology forced transfers into the same reciprocity framework, forming a closed loop of "barriers—tariffs—remedies."

WTO Path Compliant Design: Prioritize AD/CVD/safeguard measures and treaty-based exemptions, use national security sparingly to reduce "retaliation—counter-retaliation" cycles.

Scenario Examples (Workflow): 1) USTR/Department of Commerce updates "reciprocity imbalance list" quarterly → discovers a country's effective barrier index crossing threshold in key categories; 2) President issues temporary reciprocity tariffs under ERA (immediate effectiveness), while disclosing key reasons and opening 7-day opinion collection; 3) 15–30 days congressional hearings + fast voting channels start; 4) Executive agency releases formal reasons and fine-tunings, perfecting records; 5) If sued, go through CIT accelerated hearings; after 90–180 day window, automatically sunset unless Congress passes continuation resolution.

In summary, this set of solutions is "fast without losing legitimacy": #### VI. Summary: The Logical Chain of "Tariff Authority" (From Administrative Legitimacy to Government Efficiency) Diagram of the Operational Logic of Tariff Authority Fast-Fair Tariff Architecture (FFTA): ┌─────────────────────┐ │ LEGITIMACY 合法性 │ ← “No Taxation Without Representation” │ Taxation = Representation │ Congress as Source (Constitution I-8) └─────────┬──────────┘ │ Delegation ┌─────────▼──────────┐ │ DELEGATION 授權 │ ← Congress Legislates Preset Emergency Reciprocity Tariff Authority (ERA) │ - Clear Trigger Conditions │ - Reciprocity Formula & Upper Limits │ - Time Limits/Sunset Clauses └─────────┬──────────┘ │ Guardrails (Guardrails) ┌─────────▼──────────┐ │ GUARDRAILS 圍欄 │ ← Judicial and Oversight in Separation of Powers │ - Must Publicize Reasons Documents │ - 7-Day Opinions & 30-Day Revisions │ - Congressional Fast Voting Channels │ - CIT/CAFC Accelerated Hearings └─────────┬──────────┘ │ Action (Speed) ┌─────────▼──────────┐ │ SPEED 速度 │ ← Executive Immediate Trigger │ - President 180-360 Day Fast Tariffs │ - Immediate Reciprocity Snapback │ - Automatic Expiration Unless Congress Extends Legitimacy → "No Taxation Without Representation" Principle; Delegation → Congress Pre-Legislates to Set ERA; Guardrails → Procedural Justice, Judicial Review, Congressional Oversight; Speed → President Can Implement Immediately, Safeguarding National Interests #### Appendix: Outline of the Draft "Emergency Reciprocity Tariff Authority Act" (Emergency Reciprocity Authority Act, ERAA) (For Facilitating Policy Communication and Operation) Chapter One: General Provisions Chapter Two: Congressional Pre-Authorization Other countries implement substantial tariffs or non-tariff barriers;

Existence of subsidized dumping, forced technology transfers, or key industry security risks.

Chapter Three: Procedures and Oversight Chapter Four: Judicial Review Chapter Five: Supplementary Provisions Drafted on September 1, 2025, in Richmond, Heart Covenant Switch Residence

|