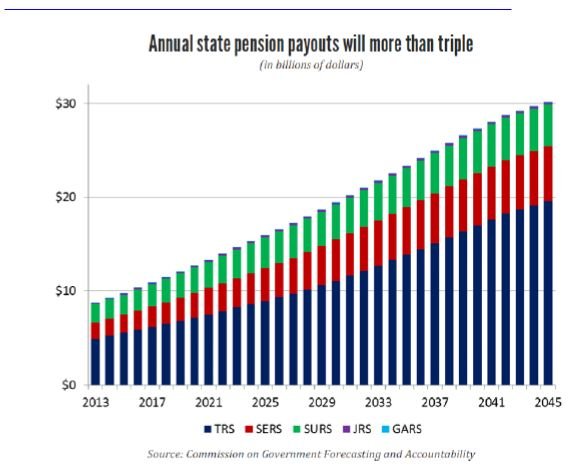

上周二 (12/3/2013), 伊利诺州议会以62 比53的投票结果,通过了历史性的公共事业员工退休金改革法案(SB1, Illinois Public Pension Reform Act),长达数年的 pension改革终于走出了实质性的一步。周三州长马上签署了该法案,但受到法案直接影响的州政府雇员工会(包括州立大学员工工会-University Professionals of Illinois, or UPI)则誓言将对此法案的合法性提出诉讼。虽然现在还无法预料诉讼的结果会如何,但这个历史性的改革法案具体条款如何,是否能如其所愿逐步解决病入膏肓的伊州退休金体系的问题,还是值得分析分析的。

1。Impose cap for "pensionable salary" -- 对“可用于退休金计算”的工资收入设立上限。以前,拿年金(annuity)的退休人员的每年退休金额是根据退休前最高工资和服务年限来计算的。如果一个教授退休前最高工资是$150K,而且总共服务了三十年的话,那么他可以在退休后每年获得退休前最高工资的80%(也就是$120K)。而目前的改革方案将用来计算退休金的收入上限设为$110K,超过这个部分的收入将不计入退休金的计算。也就是说,不管你退休前工资多高,退休后的年金最多也就是$88K一年(假设在系统内工作满30年的话)。这个改革当然对收入高的政府员工有负面的影响,而且影响不是一点点。

2。不仅如此,新的退休金改革计划还将降低退休人员每年退休金的“Cost of Living Adjustment” (or COLA) 涨幅。以前,伊州退休人员每年可以得到3%的COLA adjustment,这个涨幅的目的是用来 cover 每年的通胀(也就是所谓“生活成本增长率” )。新法案将这3%的涨幅限制于前$25K的收入,超过这个限额的部分将不再享受任何涨幅。别小看这每年3%的涨幅,如果你做一个简单的计算,就会发现,假如一个退休人员的退休年金为$72K,按照现在的每年3%的增长幅度,退休二十年后他的年收入将为$120K;而改革之后,退休二十年之后则只能拿到$85K。退休人员的实际损失还是相当大的。

4。尽管上面的几个举措都是不利于州工作人员的,但该法案有一条却是对员工有利的--那就是它提议将员工的投入分额从目前的8%降低到7%。这也是为什么伊州的共和党议员们对该法案颇有微词的原因,因为他们认为,这其实是法案的提出者(伊州民主党大佬 Michael Madigan) 企图讨好民主党大票仓--公共事业工会的做法。有评论者认为这个法案是“两边都不讨好”,这也是一个重要原因。不过,考虑到伊州是民主党的老巢(尤其是芝加哥地区),几大工会对本地选举有着举足轻重的影响,法案的倡议者也不能不考虑到工会的一些利益。

此外,还有一些 funding methods 方面的改变。比如,目前在 "Defined Benefits" 计划中的工作人员(也就是不管到退休时退休计划中的钱有多少,退休人员只按照上面所说的 formula 拿年金,从一般的概念来讲是一种”旱涝保收“的做法),有5%可以获得许可在2015年七月前选择”冻结“这部分的退休计划,而进入”Defined Contribution “的计划(但具体这5%是如何决定,被冻结的那部分计划在退休时如何领取年金,详细的措施都还没有出台)。这个做法实际上是允许一部分(当然5%这个比例在我看来有点太小了)的员工渐渐与州政府的退休计划脱钩,自己管理自己的退休金,这其实上是在向很多私营企业的做法靠拢。事实上,许多其他州政府的工作人员早就已经没有伊州这样的pension 系统了; 而伊州最近两年对退休金计划的渐进改革,已经导致很多新加入公共事业的员工选择100% 的 “defined contribution”。很多退休计划专家认为,100% 的 Defined Contribution Plan (也就是完全由市场决定退休金的回报,没有Defined Benefits 的“guarantee" )是很不保险的,尤其是考虑到伊州公共事业员工本来就不参加 social security。不过,相比许多私营企业(比如Enron)员工在公司倒闭之时,一辈子的心血完全付之东流,公共事业员工至少还是有一定的保障。所以,虽然因为这些改革自己退休后的收入会大大缩水,我觉得这些举措总的来说还是大势所趋,否则的话伊州只有一天天垮下去。当然,这个法案是否能最后真正执行,还要看公共事业工会是否能够在法庭上成功挑战它的合法性。至于这个过程会拖多久,就让我们拭目以待吧

A.自我储蓄的RRSP,不超过收入的20%, income tax-deferred, growth is tax-free; B.联邦政府的CPP,年交$2K左右,65岁后可领,max.~$1K/month; B-2.联邦政府的老年金补助,给中低收入的老人,65岁后可领,每月数百到千余; C.雇主退休金,DBPP or DCPP or combined.

说说C。DCPP一般是员工交6%,雇主等额match,投资回报自求多福。DBPP,以联邦政府的员工计划往往是取average of 5 best earning years, 2% for each year served, max.70%, age+service>=85. 员工contribution各计划不同,有free ride, 也有近10%的。

So you must be in the CALPERS system! I was working at CSU campus for a short term, so I have a little bit invested in that plan. Also because of my time with the CSU system, I will receive SS benefits (a little bit) too. So I'm going to get benefits from different sources when I retire and sure hope our plan is in good condition for the next 10-15 years :)!

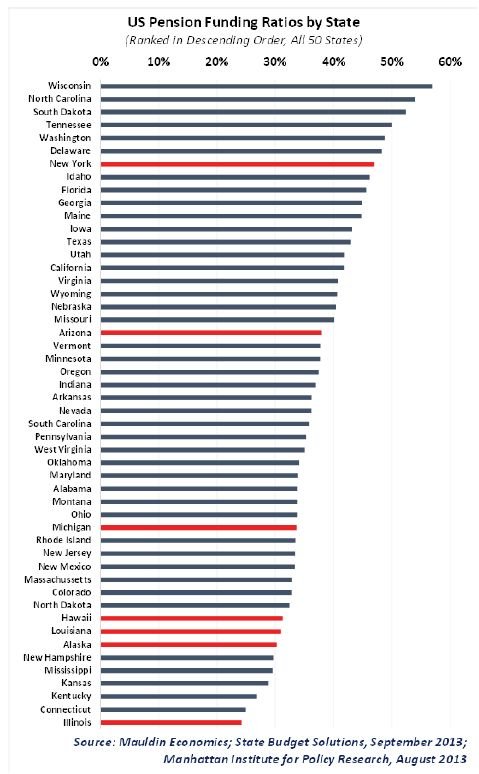

另外谢谢你补充加州州政府员工的退休金结构。曾经在加州公立大学系统工作了半年,对 的情况有点了解。照你这样说,伊州的退休制度还远远不是最慷慨的呢。这样的体系何以为继? ___________________________________ I did check the SURS report.

The plan has a balance of 14.7b, covers 199k people. In 2012, it received 1.3b as contribution from various sources including employees and the state, but benefits payouts are at 1.856b.

For the same period, the california plan that I belong to has a balance of 41.86b, covers 176k members, In 2012, it takes in 2.1b contribution, and the payouts are 2b.

另外谢谢你补充加州州政府员工的退休金结构。曾经在加州公立大学系统工作了半年,对 的情况有点了解。照你这样说,伊州的退休制度还远远不是最慷慨的呢。这样的体系何以为继? __________________________________________ Thanks, sorry that I cannot only write in English now. The california income tax brackets are pretty rediculous, and as you can see it favors the rich. Over the years, I am in this 9.3% bracket, even if I just make average salary here.

Retirement plans are very complicated. With your data, I realised that the Illinois one is poorly funded at 40+%. In California, there was a crisis several years ago in our system, since it was under 100% funded, and we started to contribute to the plan. YES, we did not contribute to our retirement plan for over 20 years, and we had something called contribution vacation.

You may hear from media that California is very poor, however, if you look at the balance of three major pension plans in California: Cal PERS, CalSTRS, UCRP, the balance is more thatn the Chinese national retirement plan.

From you posting, my conclusion that given the current funding level of SURS and other plans in Illinois, you do have a very nice pension deal.

这是美国各级政府普遍性的一个问题。 ________________________________ It will be more shocking until you hear my case: I work for an institution in California. We have a pension plan better than the Illinois one (for one, theirs is calculated based on the highest 96 months, and ours on 36 months, and the state is contributing 12% of the cost) plus full medical benefits for life for the entire family after 20 years of service. On the top of that, we have social security just like everyone else, and the employer is contributing another 7.5%.

结婚的 For earnings between $0.00 and $14,248, you'll pay 1.00% For earnings between $14,248.00 and $33,780, you'll pay 2.00% plus $142.48 For earnings between $33,780.00 and $53,314, you'll pay 4.00% plus $533.12 For earnings between $53,314.00 and $74,010, you'll pay 6.00% plus $1,314.48 For earnings between $74,010.00 and $93,532, you'll pay 8.00% plus $2,556.24 For earnings between $93,532.00 and $2,000,000, you'll pay 9.30% plus $4,118.00 For earnings over $2,000,000.00, you'll pay 10.30% plus $181,419.52

大教授, 伊州的州税是 flat tax,所以对高收入者当然不像联邦收入税那样“偏向”。好像加州的州税是类似联邦收入税,最高的 bracket 是 10.3% (for individuals with income above $1M or couples with income over $2M)。所以最近几年常听说那里的富人们不堪越来越重的税负“逃离”到其他州甚至其他国家。不过,加州的超级富豪多多,即便这样,也不会造成太大的影响。